In the first article on Bangladesh Bank we discussed the structure and role of the board and found that it needed complete restructuring to achieve independence from the government and to widen the perspective of monetary policy away from the bureaucratic stance.

The second article continued to explore the implication of an independent central banking covering the limits of central bank authorities and the need for a budget process for Bangladesh Bank independent of the executive authority.

In the third article we examined the vital work on bank inspection and concluded that it was well done, but staff could benefit from more training, anti-corruption efforts were inadequate, more attention should be focused on large loans, and a greater effort in inspection of the security of the computer systems was urgent.

Also Read - Bangladesh Bank needs to be free from influence

Also Read - Why it's important Bangladesh Bank remains independent

Also Read - What can Bangladesh Bank do to keep banks in check?

This article examines the management of problem banks.

This is an area where Bangladesh Bank has not been very successful.

We discuss what is a problem bank, the philosophy of Bangladesh Bank in handling these banks, and propose a rather different approach.

What is a problem bank?

By a problem bank I mean a bank that has a large share of non-performing loans.

I have no particular percentage in mind but any level over 10% implies that required lending rates drive profit levels to negative levels and the bank’s capital is eroding.

[1]If the spread is 4% [currently 3.2%] then with zero earnings and all bank costs covered by fees, the bank loses 2.2% on the loan.

If the NPL is 6% then the bank breaks even with the loan.

This high level of NPLs results in low earnings, inadequate capital, decline of deposits, good borrowers not renewing loans, and the steady deterioration of the bank’s performance.

To attract deposits the problem bank has to raise rates; to attract borrowers it is forced to lower lending rates.

The problem bank is caught in a downward spiral: Reduced earnings, lower capital, growing NPL, pressure on liquidity, all arising from inadequate leadership.

How does a bank become a problem bank?

The answer is simple: The quality of loans is bad.

This may be a result of bad judgment—for example concentrating too many loans in one sector; or making a large loan to a single borrower so, when he fails to repay, the bank finds itself in financial difficulties.

Banks that simply take more risk in the hope of earning high profits may be unlucky and the risky choices go against the bank.

But it may also be that the bank’s leadership is not interested in managing the bank to be a healthy financial institution but rather making money by illegal actions.

Examples of such: making loans to enterprises with relationships to directors that are not expected to be repaid; taking bribes to make loans; engaging in loans for fake imports or to fake companies.

Most problem banks arise from the illegal behavior of the bank’s management.

I consider only private banks.

State owned banks are all in terrible financial condition, but that arises from a policy decision to allow these banks to violate all rules on bank governance.

What to do with a problem bank?

The central bank’s inspection system should alert the emergence of a problem bank allowing corrective actions to be made.

In most cases the inspection system identifies the problem bank.

However, no timely and/or strong action is taken to correct the problems.

Bangladesh Bank has been unwilling to take the kind of actions that will solve the problems.

This is partly due to the lack of organizations that can make significant progress in restructuring.

But it is also due to a fear the banking system is too fragile and a failure of a single bank will trigger other failures.

This is too conservative a view and only an irrational fear.

Steps

The first step is to remove the Board and appoint an officer to run the bank.

Often senior officers in the bank may also be asked to leave.

A careful analysis of the loan portfolio will establish the depth of the problem facing the bank.

It is important to have an independent audit carried out by a good auditor.

The correction action is always the same: work hard on loan recovery and determine if there is any prospect of bringing the bank close to meeting capital adequacy.

If so, then the central bank can contribute to the capital of the bank to bring the position up to meet the required capital.

A program to retain depositors is needed to prevent or limit a run on the bank.

This requires creating public confidence that the central bank will protect the deposits.

This is partly the result of the deposit insurance and partly strong public statements by the central bank.

However, if the problem bank is to be rescued one has to stick to the law and the central bank has to believe that it can achieve the needed results.

A cost cutting program must be introduced to reduce as much staff as possible and to close branches that are not collecting enough deposits.

An example of a rule for continuing a bank branch: Annual change in deposits should be large enough that the interest earned if 90% of these deposits are lent and earned at the lending rate is enough to cover the staff costs and the interest paid in one year for the increased deposits.

When all of this is done the central bank can then sell its shares to the public; a strategic buyer must be found who will take over the operation of the bank and rebuild its loan portfolio.

The central bank has never been able to come out with a good result from a problem bank.

The main problem is that the closure of a bank was never considered an acceptable choice.

With this solution off the table the hapless central bank was left in an impossible position.

In one case foreign investors were gulled into buying the bank but were left with a losing proposition with the bank simply dead but no one issuing a death certificate the new owners were not allowed to go to court.

In another case the bank just continued to make poor loans and the Board looked at the benefits while Bangladesh Bank stood by.

Problematic banks

There are at least three private problem banks at present (NPL>10%).

These banks should not be turned into government banks.

Everyone should have learned their lesson from the disaster of Basic Bank.

Bangladesh Bank should not trick foreigners into investing with promises of forbearance.

An effort should be made to clean up the problem bank’s portfolio, described below.

But the outcome must bring the bank close to capital adequacy so that a loan or capital contribution from the central bank will bring the bank into compliance.

If this is not feasible the bank should be closed.

To properly manage problem banks several actions are needed:

1. A department of Bangladesh Bank should be established responsible for managing problem banks.

Its duties should also include managing the premiums collected from deposit insurance.

2. This section of Bangladesh Bank working with the off-site inspection teams should identify banks which might be considered problems.

These banks should already have a central bank representative on the board; if not, one should be appointed immediately.

These representatives from the central bank should be under the problem bank department.

3. The condition of the problem banks should be reviewed in the central bank’s monthly Board meeting.

The problem bank department should work out a strategy for taking control of the bank and have it ready for use when necessary.

4. The deposit insurance limit should be increased so that the insurance coverage of deposits is much greater than at present. The current limit is only Tk1 lakh.

All banks would then pay the necessary premium.

The funds available from deposit insurance should be managed by the problem bank department.

In particular the funds can be used to support the position of a problem bank.

Raising the limit to Tk10 lakh would protect most deposits by private persons and cover about 70% of private deposits.

5. An asset recovery organization should be established independently of the central bank.

A special tribunal should be established that is tasked with hearing the case for any loan that is handed over to the asset recovery organization.

All other cases concerning the loan would be combined with the case brought before this tribunal.

If a recovery action is approved and an appeal is made to the High Court then the defaulting borrower must deposit say 75% of the amount due with the tribunal for asset recovery court for the appeal to go forward.

When Bangladesh Bank takes over a private bank it will take a loan considered uncollectible in a reasonable time and with reasonable effort and give it to the asset recovery organization.

That organization would make every effort to collect the loan through the tribunal.

A rule such as 30% of the collections will be distributed as bonuses to persons employed in the asset recovery organization and the remaining 70% given to the central bank.

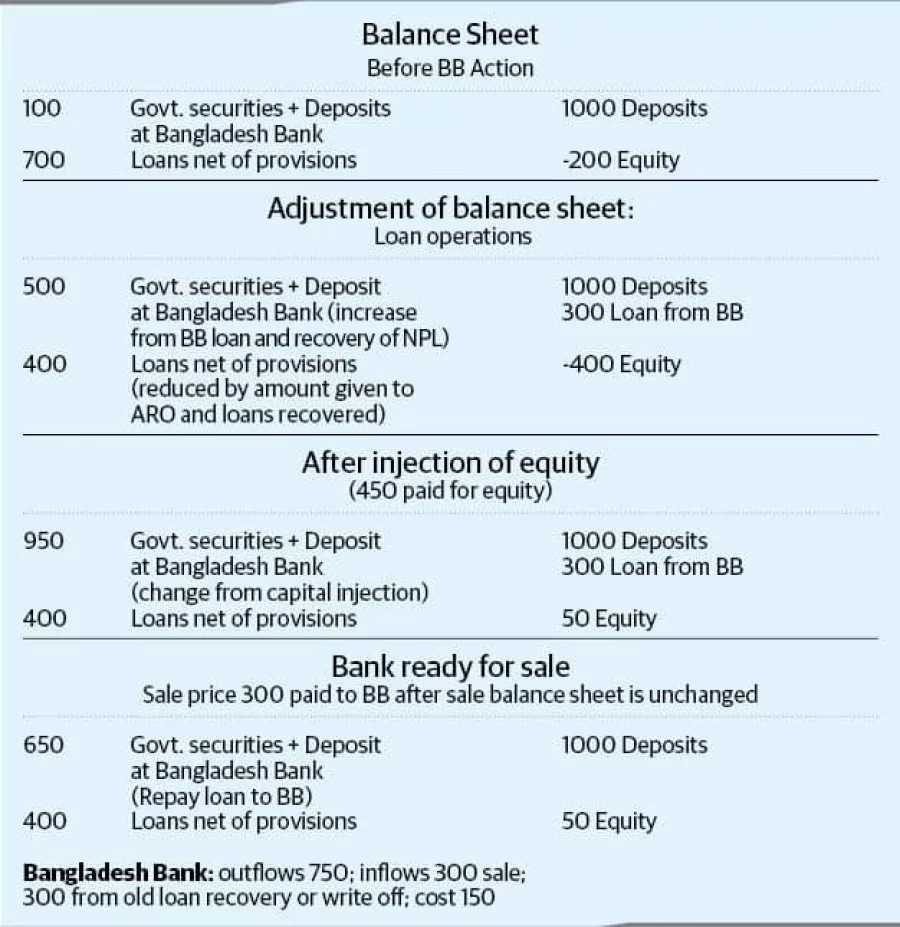

Box 1 sets out an example:

The bank is insolvent.

Existing share values marked to zero.

In the first step Bangladesh Bank makes a loan of Tk300 to give bank some flexibility, a recovery drive raises Tk100; Tk200 are written off and given to the ARO.

This changes the equity to Tk-400.

Next the BB buys Tk450 of equity issued by the bank.

This changes the equity to Tk+50.

Finally the bank is sold to new owners for Tk300.

Bangladesh Bank has spent Tk750 and received Tk300 for a cost of Tk450.

Of this Tk300 is a loan the restructured bank will repay.

Bangladesh Bank loses Tk150.

If the bank had closed and 400 loans were recovered then the depositors would lose 500.

This method will reduce the assets of the bank as loans are removed from the balance sheet.

This reduces the capital of the bank.

After the loan recovery effort is completed the balance sheet will have a hole.

This will partly be covered by the purchase of shares by Bangladesh Bank and partly by a loan from the central bank to the problem bank. The box illustrates these steps.

The bank is ready for sale with a very liquid position, loan portfolio purged of loans unable to collect, and with adequate capital.

Its earning position is weak but it is able to make good loans and raise the profitability of the bank.

The surplus liquidity of 550 can be partially loaned (say 400 is lent) and should earn 8% (2% on lending) or approximately 16% on equity of 50.

If it is impossible to carry out this type of operation then the bank must be closed.

Even if closed one still needs the Asset Recovery Organization to collect from the defaulters.

Forrest Cookson is an economist who has served as the first president of AmCham and has been a consultant for the Bangladesh Bureau of Statistics.

[1] The cost of lending (interest rate) must include in every loan funds needed to cover the unpaid loans. If x is the amount to be collected from every loan, 10% of the loans are non-performing, A is total loans, and 80% of NPL are bad/loss then

Amount collected to cover all loan losses

.9Ax

The losses from bad loans are

.1A(.08)(.7) = .056A

where we assume 30% of the loans can be recovered from collateral. We ignore interest lost is

Thus .9Ax =.056A

The loan loss provision is 6.2%!

At 6% bad loans the loan loss provision is 3.6% greater than the current spread.