Consumer prices in Bangladesh are currently at levels never seen before. Official inflation numbers put May 2023 inflation at 9.94% which is the highest in a decade. Some experts believe the actual number to be even higher.

What is driving inflation in Bangladesh? There are two strong theories going around in newspapers and social media. First is the idea that a huge amount of money printing is happening along with debt monetization by the government. The other popular theory alongside that was the aftermath of the Russia-Ukraine war that started in early 2022 caused inflation.

Is money printing the main culprit?

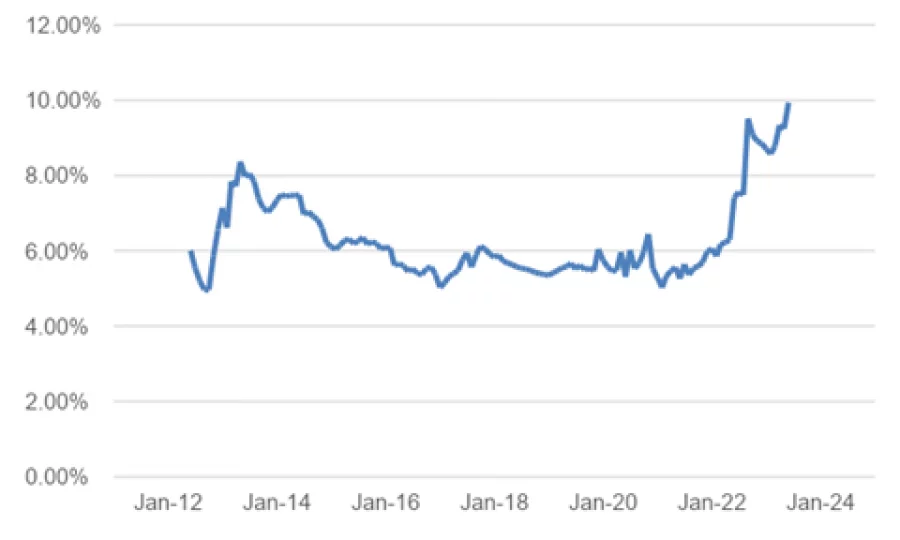

Figure: Money Supply Growth

Data dispels the first argument completely. Broad Money growth aka M2 growth stands at 9.46% as of May 2023. Broad money growth peaked at around 14% during the pandemic period, when Bangladesh Bank, along with rest of the central banks around the world, went for a monetary stimulus. However, since then money supply growth had decreased to a number between 8-10%.

Compared to the highly expansionary years of 2009/10 where M2 growth was as high as 24%, the current numbers are significantly lower. Also considering Bangladesh's nominal GDP growth number a sub 10% money supply growth is definitely quite reasonable.

The recently announced Monetary Policy Statement also further strengthens this argument. After a long time, lending rates have been allowed to adjust and immediately afterwards treasury bill and bond yields have moved up. There is no doubt Bangladesh is running a conservative monetary policy at the moment.

Is it a supply side problem?

The Russian invasion of Ukraine started in February 2022. This event was widely considered a major reason for inflation. Yet, the IMF All Primary Commodity Price Index was up 47% between February 2021 (Index=138) and February 2022 (Index=203). This means commodity prices were on the way up even before the war started. After the start of the war, the index went up another 19% to peak at 242 in August 2022. As of May, the index value stands at 158.3 -- a drop of 35% from the peak.

This means that while the war did have an impact in 2022, the commodity markets were hot even before that. In addition, by late 2022 global prices had started to come down aggressively.

Retail prices in Bangladesh diverged completed in the last 10 months or so. Consumer prices kept increasing in Bangladesh even when global prices fell. Prices of a number of products in Bangladesh and our neighbouring country India became ridiculously different.

Tracing the timeline for inflation movements

We had already established that aggregate demand is weak and hence the inflation we are experiencing is not demand pull. It is clearly cost-push in nature.

The early acceleration in inflation was driven by global commodity price hikes before and after the war. However, in the second half of 2022, when global commodity prices started softening, depreciation of the Bangladeshi taka was the main driver of price hikes.

If we fast forward to 2023 and particularly the period between the two Eid festivals, neither did Bangladeshi taka depreciate much, nor did global commodity prices rise. Yet prices of many essentials jumped sharply. This is the period where I would attribute the inflation purely on supply shortages caused by a lack of dollar availability.

Such supply shortages allow hoarders to extract significant economic profit. There is also the question of "margin of safety." Most importers are having to go for deferred LCs, often having to wait around 7-8 months to settle their dues. This leads to substantial uncertainty on the dollar rate which they may have embedded in their product pricing right now.

Concluding thoughts

Post 2012 inflation in Bangladesh (both BBS reported and what we felt as a citizen) was low all the way until 2020. Low global commodity prices and also a strong Bangladeshi taka played a role. The Bangladeshi taka has been overvalued since 2018 and it kept inflation low in those years.

In 2022, the country was hit by a double shock of exchange rate adjustment and sharp commodity price hikes resulting in a major inflation shock.

Fortunately, I can see light at the end of the tunnel. Bangladeshi taka has depreciated significantly and my personal view is that it is near its fair value. Global commodity prices have declined after a series of interest rate hikes by global central banks. Bangladesh's current account balance on a monthly basis is starting to print positive numbers (4 out of the last 5 reported months had surplus).

While it may be slightly early to predict, we are seeing some trend reversals in our FX Reserve position. Improving dollar liquidity will most definitely lead to reduction in consumer prices. We have already seen how imports from India have led to reduction in Onion and Green Chili prices. We will see the same across the board if our dollar liquidity position improves.

Given the demand dampening steps such as currency depreciation, energy price hikes and most recently adjustment in bank lending rates, I am hopeful of a better outlook in the second half of this year.

Asif Khan, CFA is Chairman of EDGE AMC Limited. All views expressed are his personal opinions.