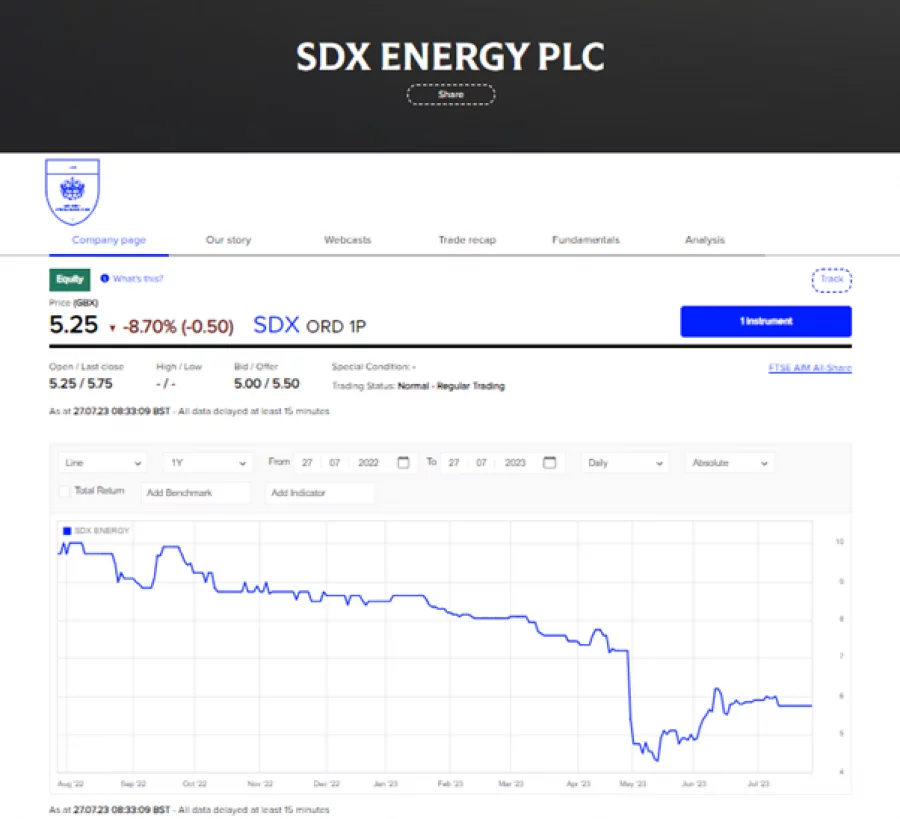

SDX Energy (LON: SDX) shares are down 9% on the issuance of a convertible bond. That they're having to pay 15% - yes, 15% - on a convertible does show that there's a certain hunger for working capital here. But then we knew that, it just underlines how difficult the situation had become.

The announcement from SDX: “SDX is pleased to announce that, following the securing of higher gas prices, the Company has secured financing to expand its Moroccan gas production. The syndicated convertible loan agreement with Aleph Finance Ltd for up to $3.25 million (the "Convertible Loan") of which an initial amount of $2 million has been drawn and will be immediately used to reduce outstanding debt to the European Bank for Reconstruction and Development ("EBRD"), pay critical service providers to accelerate the Moroccan drilling campaign and for general corporate purposes. The Convertible Loan enables the Company to move the business forward, towards an energy transition strategy, as it continues with the process to sell its Egyptian assets with a view to deliver value to shareholders.” The Egyptian business has been hamstrung by the difficulties being placed in the way by the bureaucracy there. Pricing, the ability to repatriate earnings (and so pay debts), convertibility of currency and so on. These all should be covered in the varied investment treaties but it's always possible for a bureaucracy to cause problems.

SDX Energy share price from London Stock Exchange

That's what caused that share price drop at SDX in May, those Egyptian problems becoming apparent. But they've been able to get the price of their Moroccan gas up and that does look a better jurisdiction to be looking in as well. So, all is well?

Except look at the price they're having to pay for that money: “The syndicated Convertible Loan is unsecured, convertible at any time at the option of the individual lenders and repayable 364 days after the initial drawdown of the Convertible Loan is made. The conversion price is approximately 4.5 pence per Ordinary Share (or, if lower, the lowest issue price for any Ordinary Shares issued during the life of the Convertible Loan). If conversion occurs within ten business days of maturity, the conversion price is approximately 6.6 pence per Ordinary Share.

Interest of SOFR+15% on the Convertible Loan”

The conversion price is around market, that the conversion price adjusts if there's a rights issue, that's all fine. But 15% above base (which is about what SOFR is). That's a heck of a price to have to pay for money. Around 20% overall - and on a convertible bond. Sheesh.

It's good that SDX has been able to get the money, But they're sure paying for it.