Peak Rare Earths (ASX: PEK) (OTCPK: PKTRF) is up 16% Thursday morning on the announcement that they're going to go ahead and sign the agreement in Tanzania. That might sound a bit much of a move just for signing something we knew was coming. But on the other hand no such agreement is ever worth anything until it is actually signed - so we've derisking here.

Peak Rare Earths is to mine bastnaesite in Tanzania and upgrade to a concentrate at the site. There's an agreement to send this into China for processing, with Peak being paid the concentrate price. There's also the opportunity, later, to upgrade Peak to having its own rare earth processing and separation plant on Teesside in the UK. Given the current rare earths excitement this seems a logical enough process, take a bite at a time and evaluate the next step after having done so. After all, trying to do every thing at once (as Pensana has tried to do) can lead to a distressing running out of money.

So, much of their planning seems entirely sensible. However, it's worth having a look at their details. From their presentation:

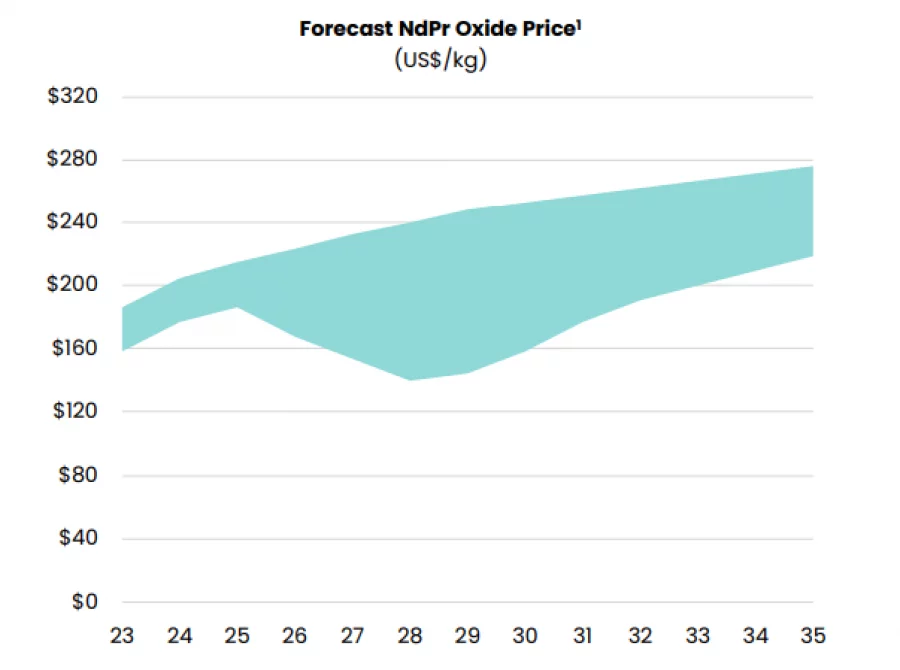

Price assumptions from Peak Rare Earths

That they use only the Nd/Pr price is a usefully simplifying assumption given their ore, that bastnaesite. The Dy and Tb values will be so low as to be nice additions if they happen but not vital considerations. However, the entire project does depend upon those prices:

Price assumptions from Peak Rare Earths

Now here's the thing. It really was only a few years back, less than 5, that Nd/Pr was selling at $40 a kg. Yes, we can make assumptions about future demand and supply and forecast continually rising prices from here. We're less certain that that's exactly what is going to happen. As we've noted talking about OD6, Australian Rare Earths and Heavy Rare Earths there's an entirely different mineral and source coming up in the outside lane - ionic clays. We're really deeply uncertain - uncertain note, not certain - that the Nd/Pr price is going to hold up like that. The potential supply of rare earths is a lot higher, we think, than many other plans seem to assume.

This isn't to say that this Tanzania plan by Peak Rare Earths won't work. It is just to insist that any evaluation has to start with an idea of that future of the Nd/Pr price. Everything then follows from that.