Albemarle (NYSE: ALB) stock looks like one of those nobrainers. The world is screaming out for more lithium to feed the electric vehicle revolution. Albemarle is one of the largest extant lithium miners, profitable, dividend paying and in general looking just fine. But this is to miss something about the mining industry. As Elon Musk has pointed out there's no conceptual shortage of lithium. There's lots of it out there, vastly more than humanity would ever want to use. The only even conceptual possible shortage is of people with the mines in action to extract it. And, well, this is something that capitalism is very good at indeed - producing more of whatever it is that people want in volume.

Thus we should perhaps view ALB stock as a leverage bet on the lithium price itself. For Albemarle is, like all miners, a commodity producer. Well, obviously, metals and minerals are commodities. But there's a further economic meaning here, which means “price taker”. The price of lithium does not depend upon what Albemarle does, nor what its costs are. There's also little way for Albemarle to differentiate its lithium from that or any other miner - or from the flood of recycled material that will arrive in time. Therefore ALBs' margins, profits, depend entirely on what the lithium market price is. And that is not determined by Albemarle but by how many other people open lithium mines.

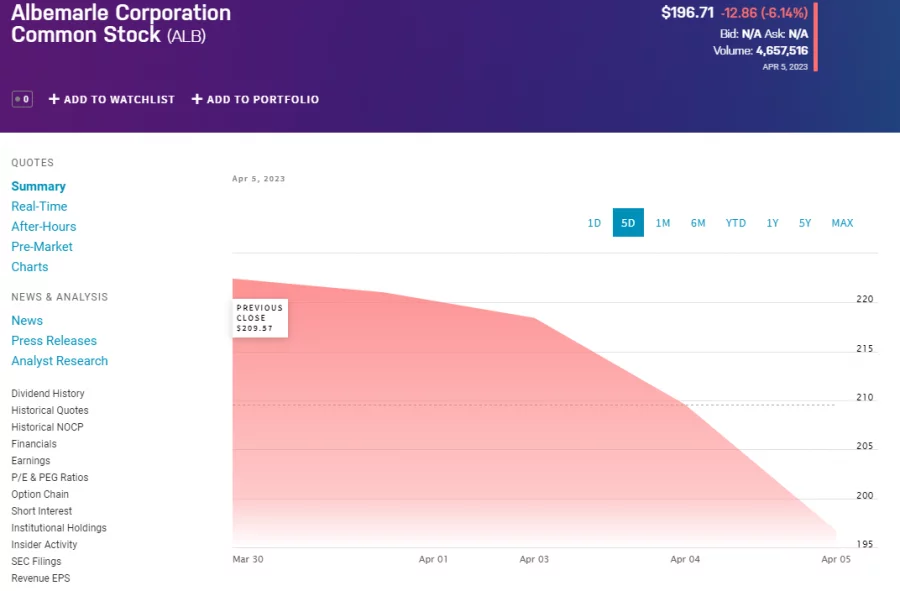

Albemarle share price from NASDAQ

Which is what gives ALB a medium to longer term problem. It can take some years to open a new mine. But look forward a few years, how many of those new mines will be open? BofA Securities has downgraded ALB on the basis that more such mines will be open in the future than we've all been imagining will be. After all, the lithium spot price is down 40% already in recent months. Albemarle will still be profitable at much lower prices than today so that's not the whole concern here.

What will worry bears on the lithium price is the obvious strategy being pursued by the Albemarle board. There's that bid for Liontown for example. If lithium prices recover into the future then that Liontown price looks like something of a steal. But what if many more mines come online and so the Li price falls back to something like historical average? As above, ALB's current mining would still be OK. But it would also have paid out real cash to buy lithium deposits at the top of the market. That wouldn't be good at all.

Albemarle's obvious strategy - expanding resources and reserves at current market prices - works really well if the lithium price recovers and moves upwards again. It's a path to a great deal of financial pain of the lithium price falls back to historical levels. So, the bet is clearly, what do we think lithium prices are going to be in the middle distance future? Given our experience in minor metals markets we think the possibility of significantly lower is quite high. But that is an opinion, not a fact.