The world is moving towards a cashless economy, and Bangladesh is no exception.

And in today’s Bangladesh, where online stores are replacing brick and mortar shops, people also favour paying digitally and financial institutions are catching up to the trend.

Interestingly, while we are still working to enable easier access to financial services for every person, digital financial transactions are also exhibiting robust growth, replacing conventional banking transactions.

If we only take internet banking, for example, in the first quarter of 2022, Bangladesh witnessed over 14 million internet banking transactions, which is double the number of transactions in the first quarter of 2021.

In fact, in three years, internet banking transactions have increased by more than five times, which was only 2.7 million in the first quarter of 2019.

If we look at mobile wallets, 2019 experienced 2.5 billion MFS transactions, which rose to almost 4 billion in 2021.

This trend is also observed in wage earners’ remittances received by Bangladesh.

Though the market was and is still dominated by cash pickup, expat Bangladeshis and their beneficiaries are gradually adapting to digital channels.

Especially during the pandemic, when physical outlets of money transfer operators were closed worldwide, the benefits and convenience of cashless remittance were visible.

At the same time, scheduled banks have put commendable efforts into drawing remittance directly to accounts, with some banks offering an additional incentive on top of the government incentive.

Major MFS providers have also promoted similar offers to motivate customers to get their remittances directly to mobile wallets.

For a deep dive into what banks are doing to grow the cashless remittance portfolio, let us look at Brac Bank, where we have achieved exceptional results in the digitalization of remittance.

Transactions

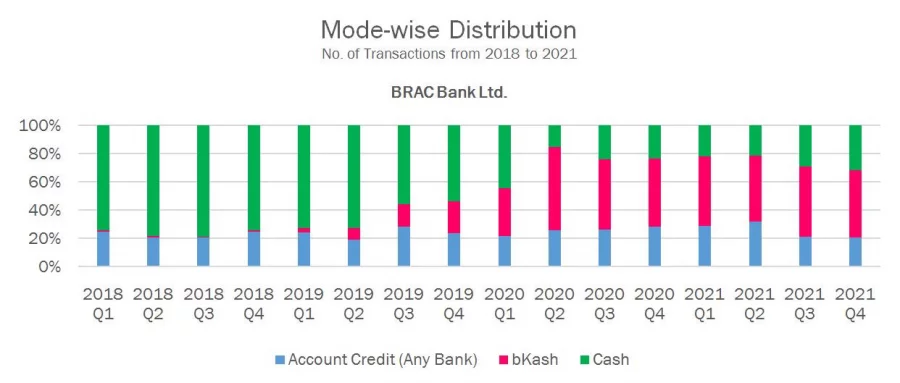

In the first quarter of 2018, 75% of Brac Bank’s total number of remittance transactions was executed in cash.

But in less than three years, the bank has continuously onboarded a commendable number of customers to digital remittance channels.

This was reflected in the last quarter of 2021, when only 25% of all remittance transactions processed by Brac Bank were cash-based.

That means 75% of the bank’s total number of remittance payments is now being disbursed in completely cashless channels. And that too in a market where more than half of the amount received as formal remittance is paid out in cash.

For each cash payment, however, beneficiaries need to travel long distances from their households (often in remote rural areas) to bank branches located around city centers and carry large sums of cash back to their homes.

It costs the beneficiaries money and time to travel to a bank branch and back home each time cash is sent from abroad.

The endless list of necessities for digital remittance does not end there.

While remittance costs are a significant concern for migrant workers, cashless channels offer the service at the lowest cost.

For example, Brac Bank does not charge any service fee from any partner exchange house for each remittance payment directly credited to its accounts.

On top of that, Brac Bank also offers more competitive exchange rates in digital channels to promote cashless remittance.

Considering all these, the cost of remittance for the migrants is significantly reduced if they switch to digital payment.

With the aim to provide access to cashless remittances for all its customers around the country, BRAC Bank embarked on its journey toward digital remittance long ago. While the bank is now observing only good traction in digital remittance channels, its digital transformation journey started several years ago.

The bank has invested heavily to build a state-of-the-art technological backbone that can support the full-scale digitalization of our service delivery channels and internal processes and systems.

The first step was to develop an internal infrastructure that could support hundreds of automated payments daily, round the clock.

With that motto in mind, Brac Bank developed its in-house remittance application mRemit, which is directly connected to the payment systems of all its partners worldwide to facilitate real-time transactions with no human intervention.

To expand its portfolio of cashless payments, Brac Bank also needed to onboard partners specializing in digital remittance.

Some leading global exchange houses are traditionally cash-focused, and most of their customers are also cash-based.

Forging partnerships

That is why, along with these industry leaders, Brac Bank gradually developed partnerships with new-age money transfer operators and fintech-based exchange houses with strong digital remittance disbursement capabilities in the past few years.

One last challenge in this frontier was educating the customers.

Migrants and beneficiaries generally lack adequate financial literacy and are more accustomed to cash-based transactions and traditional savings methods.

To address this, Brac Bank launched widespread financial literacy programs around the country as well as abroad. In the rural areas, the bank hosted Customer Meets.

Outside the country, Brac Bank organized seminars and workshops for migrants to educate them on the benefits and convenience of digital financial services.

The bank also circulated audiovisual tutorials on its social media platforms to make it even easier for the customers to understand how to leverage the digital remittance services of Brac Bank.

The gravity of these initiatives became truly discernible when the pandemic hit the world near the end of 2019.

As the world started to witness its socioeconomic repercussions, an April 2020 estimate by the World Economic Forum projected the flow of global remittances to decline by 20% in 2020.

Amid the worldwide shutdowns, the top bottleneck was the limited availability and access to remittance services.

Not considered essential businesses, many exchange house agents were not operating.

At this juncture, digital remittance presented a welcome alternative to in-person interactions at physical outlets.

And as we have observed, the remittance inflow to Bangladesh in formal channels during the pandemic was not halted at all, but against all odds it increased many folds.

While cash transactions at branches nosedived because of worldwide lockdowns, remittance payments through bank accounts and mobile wallet modes soared during this period propelling the wheel of the economy.

While the journey toward digitalization will continue, the banks do not disregard the importance of traditional payments too.

When beneficiaries visit branches or agent outlets for a cash payout, the banks get the opportunity to connect with them and explain the features and benefits of digital remittance.

That is why banks are adopting the phygital strategy, where the customers are served at brick and mortar branches and through digital platforms per customer choice.

The author is a senior banker who specializes in remittance and Probashi banking