Bangladesh's banking industry is navigating one of its most severe systemic crises since independence.

A sharp increase in classified loans, restructured credit facilities, and bad-debt write-offs has severely weakened the industry's financial baseline.

This deterioration is clearly visible across the industry's net earnings, capital adequacy metrics, and core stability indicators.

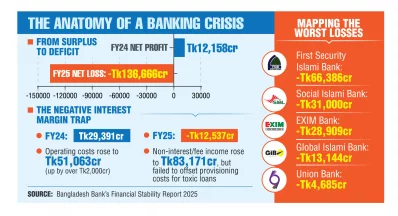

According to the newly released Financial Stability Report 2025 by Bangladesh Bank, the banking industry posted a consolidated net post-tax loss of Tk136,666 crore for 2025.

This marks a significant downturn from 2024, when the industry generated a net consolidated profit of Tk12,158 crore.

This represents the first time in recent financial history that the country’s entire banking infrastructure has recorded a net negative balance sheet.

Financial analysts point out that while forbearance policies and lenient regulatory rules previously masked the true volume of non-performing assets (NPAs), current accounting disclosures are revealing the true scale of the risks.

Consequently, long-standing concerns regarding the financial health of commercial lenders have now materialized in official performance metrics.

The central bank report highlights a major drop in the industry's net interest income (NII), which fell to negative Tk12,537 crore in 2025.

This negative margin indicates that commercial banks paid out more in deposit interest to savers than they generated in active interest income from their outstanding loan portfolios.

This performance stands in sharp contrast to 2024, when the industry maintained a positive net interest income of Tk29,391 crore.

The swift contraction within a single fiscal year underscores the structural vulnerabilities facing commercial loan books.

Non-interest income streams—including commission, brokerage, and fee-based services—showed some resilience, growing from Tk63,861 crore in 2024 to Tk83,171 crore in 2025.

However, this non-funded revenue growth was insufficient to offset the heavy provisioning requirements triggered by rising default loans.

Concurrently, operating expenses—driven by higher administrative costs and staff salaries—expanded by over two thousand crore to reach Tk51,063 crore.

These factors combined to push pre-tax losses to Tk124,284 crore, ultimately leading to the historic post-tax net deficit of Tk136,666 crore.

While individual bank performance metrics are kept confidential within the Financial Stability Report, data from the state-published Activities and Statistics of Banks and Financial Institutions reveals that the ten lowest-performing lenders accounted for a combined loss of Tk154,745 crore.

Notably, the top five loss-making entities consist entirely of recently merged Shariah-compliant Islamic banking institutions:

- First Security Islami Bank: Recorded the largest individual deficit with a net post-tax loss of Tk66,386 crore.

- Social Islami Bank: Posted a net loss of Tk31,000 crore.

- EXIM Bank: Registered a deficit of Tk28,909 crore.

- Global Islami Bank: Recorded a loss of Tk13,144 crore.

- Union Bank: Logged a net post-tax loss of Tk4,685 crore.

Other commercial operations, including AB Bank, IFIC Bank, National Bank, Premier Bank, and Padma Bank, also reported substantial balance sheet deficits during the same review cycle.

Distressed assets

The primary driver behind the industry's financial distress is the rapid expansion of non-performing and impaired loans.

Bangladesh Bank data shows that total distressed assets reached Tk1,087,590 crore by the end of 2025, representing 59.73% of all outstanding loans in the banking system.

Compared to the previous year's asset log of Tk756,553 crore, distressed assets grew by Tk331,037 crore within 12 months.

This metric tracks the combined volume of officially classified non-performing loans (NPLs), the unrecovered portions of rescheduled loan accounts, and legacy written-off books.

At the close of 2025, the country's total outstanding loan base stood at Tk1,820,915 crore, with NPLs accounting for Tk557,217 crore, rescheduled outstanding credit at Tk446,894 crore, and written-off assets holding at Tk83,479 crore.

As a direct result of asset quality deterioration and mandatory provisioning write-downs, the banking industry's consolidated capital framework experienced a severe decline.

Under international Basel III guidelines, commercial banks are expected to maintain a minimum Capital to Risk-Weighted Assets Ratio (CRAR) of 12.5%.

However, by the end of 2025, the banking industry's consolidated capital adequacy ratio dropped to negative 2.64%, down from a positive position of 3.08% the previous year.

The capital shortfall is particularly visible within the Shariah-compliant segment, where the consolidated capital adequacy ratio for Islamic banks plunged to negative 43.18% at the end of 2025.

Furthermore, several Islamic banks missed key regulatory targets for liquidity management, including the Liquidity Coverage Ratio (LCR), Net Stable Funding Ratio (NSFR), and statutory Investment-to-Deposit Ratios (IDR).

To ease balance sheet pressures, financial institutions restructured a record Tk170,503 crore worth of loans in 2025.

This represents a significant increase from the Tk85,679 crore rescheduled in 2024 and the Tk91,221 crore adjusted in 2023.

Despite the scale of these adjustments, the underlying rate of loan defaults continued to rise, indicating that repeated restructuring without operational improvements has expanded overall portfolio risk rather than resolving default issues.