OSB (LON: OSB) shares are down 24% today. OSB shares dropped because the company management has revealed a problem with revenue recognition. Sometimes to often enough revenue recognition becomes one of those things that kills a company - or at least the share price. People, say - and naming no names - selling hardware but claiming that it was much higher margin software. Or packing the wholesale channel to boost year end results then finding that sales plummet as that extra stock takes time to sell on retail.

Here at OSB it's not, in fact, any of those things which are clearly wrong in and of themselves. Rather, the behaviour of customers has changed and this then impacts because on the way that OSB recognises revenue. “In line with IFRS 9, the Group applies the effective interest rate (EIR) methodology to revenue recognition. This method seeks to recognise interest income evenly over the expected life of a mortgage, based on expected future cash flows and taking into account behavioural aspects, including time spent on the reversion rate, in addition to contractual terms. The Group uses observed trends in customer behaviour to periodically update modelled assumptions for the expected time spent on the higher reversion rate. Once a change in customer behaviour becomes apparent, and is expected to persist, the Group is required to recognise an immediate adjustment to the carrying value of the loan book through net interest income.”

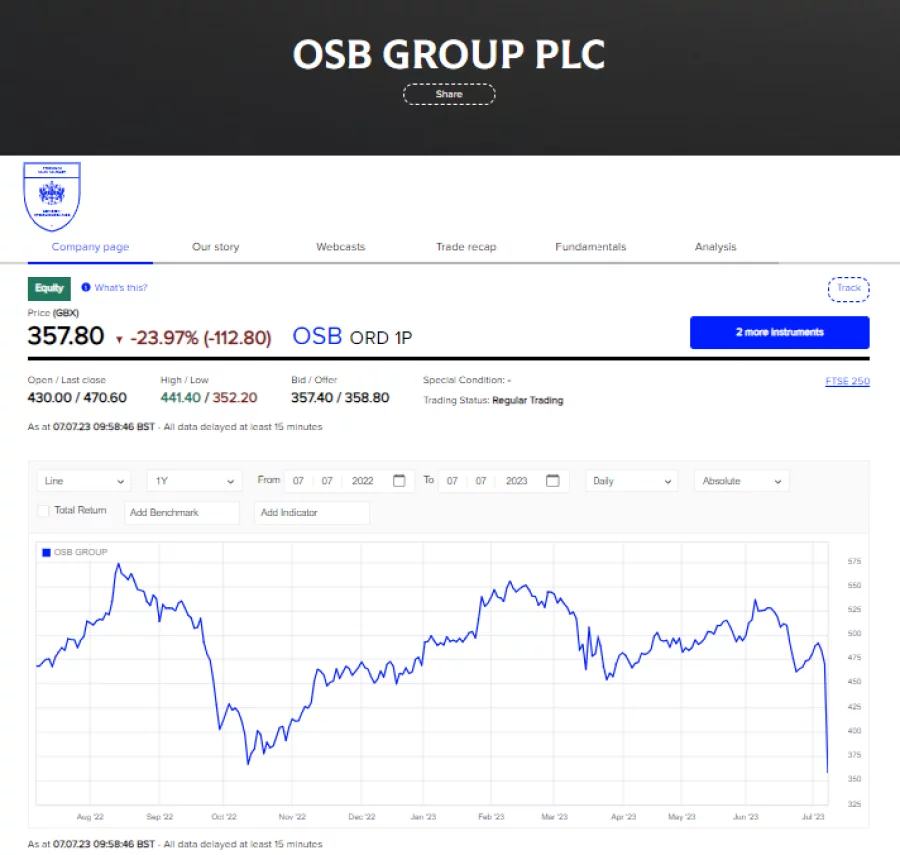

OSB Group share price from London Stock Exchange

To put that explanation into English. OSB specialises - in part - in buy to let and landlord mortgages. Most of these come with a year or three of fixed interest rates. Once that period comes to an end the mortgages flip to floating rate mortgages. The margins on the floating rate seem to be rather better.

Also, OSB recognises the revenue from any particular mortgage over the life of that mortgage - or rather, the likely life.

What's been happening is that as the fixed rate deals have been coming to an end the mortgagees are refinancing faster than they used to - leading to a shorter period on those more profitable rates. Because of the way that revenue is recognised this means OSB now has to revalue the entire mortgage book - that's a heck of a hit to the balance sheet: “an estimated adverse EIR adjustment of £160m to £180m on an underlying basis in the first half of 2023.”

Not nice and not fun but it is the right thing to do. Far from this being dodgy accounting this is actually the right way to do revenue recognition. But it does mean that the behavioural change therefore hits results in one big bang rather than filtering through into earnings over time.