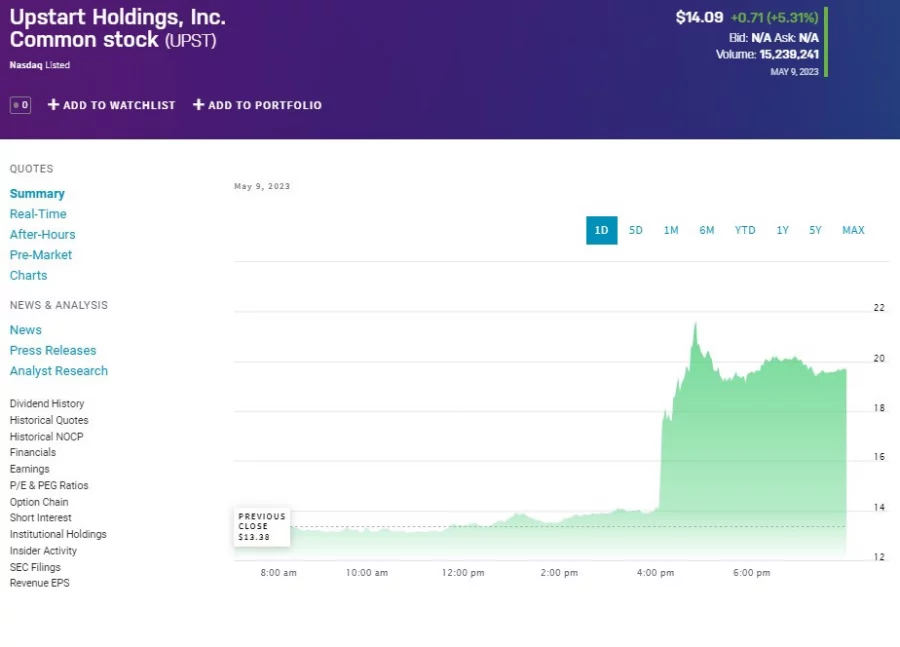

Upstart (NASDAQ: UPST) stock was up 40% last night postmarket after it announced Q1 results. Those beat expectations, which is a part of what drove UPST higher. There were also confident predictions of Q2 adjusted EBITDA being at breakeven - which would be a nice change for the company. So, all is looking good, right? Certainly, things should be looking good but it's possible to have a nagging little doubt here.

The basic idea, as has been pointed out before, has substantial merits. Once we get to any scale - so when considering any form of consumer lending for example - then lending decisions are really pattern recognition. Credit scores are pattern recognition after all - folk who did these sorts of things in the past are likely to do these other sorts of things in the future. Unless there's going to be a live human being checking every fact on offer any large scale set of lending decisions will be about patterns, recognising the tells of those likely to repay and those likely not to.

OK, that's great, and what do we know about Artifical Intelligence? That it's really a pattern recognition engine. When we drill right down that's what AI is. So, we can see the obvious attraction of setting an AI to make lending decisions. AIs are good at pattern recognition, lending decisions are pattern recognition, it should work. And as a concept sure it should. That's pretty much the Upstart offering. A platform through which lenders can use the corporate AI to make lending decisions in return for a fee.

Upstart Holdings stock price from NASDAQ

So, Q1 results beat expectations, Q2 might bring adjusted EBITDA to flat, what's not to like?

Well, there is the one more little feature here. Upstart used to be just the platform. Providing the tech and taking a fee for it. Which is one business model. Another is that Upstart actually make the loans. Keep the lending decisions on its own books - hey, why let the banks make all the interest, right? And Upstart has been increasing its exposure here: “Will the company continue to utilize its balance sheet to retain more loans? Notably, Upstart's loans held on its balance sheet surged to $883M at the end of 2022, up from $143M at the end of 2021. It represented nearly 46% of its asset base,”

Hmm, well, views will differ here. But are we really sure that the top of the credit cycle is really the place to be taking more credit risk onto the balance sheet? Of course, if the AI really works in selecting only the best credits then this won't be a problem. But does it?